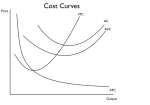

1. Cost Theory (total, fixed, variable costs; calculating costs):

Total cost – the sum of both the fixed costs and the variable costs. Total Cost (TC) = Fixed Cost (FC) + Variable Cost (VC).

Fixed cost – costs that do not change in the short run, even if output is zero. For example, rent that you need to pay for using a certain area of land will always be there, no matter how much of your product you produce.

Variable cost – costs that change depending on the level of output. For example, if we own a shoe factory, if our original output was 100 shoes, but then we increase our output to 200 shoes, we would need to increase our labor force to compensate. Therefore, labor would be a variable cost in this case.

Total product – the total output of a firm.

Average product – the total output of a firm divided by the units of the variable factor. Average Product = TP/V

Marginal product – the change in the total product (output) for every additional unit of a variable factor used. Change in TP/Change in V

Average fixed cost (AFC) – the fixed cost per unit output. Average Fixed Cost = Total Fixed Costs (TFC)/Output

Average variable cost (AVC) – the variable cost per unit output. Average Variable Cost = Total Variable Costs (TVC)/Output

Average total cost (ATC) – the total cost per unit output. Average Total Cost= Total Costs (TC)/Output

Marginal cost (MC) – the increase in total cost of producing an extra unit of output.

2. Law of diminishing returns:

Law of diminishing returns – the economic idea that states as more and more of a variable factor are added to fixed factor, output will rise initially but will eventually fall.

3. Short-run:

The short run – the period of time in which at least one factor of production is fixed. Over this time period the firm can only expand production by using more of the variable factor.

4. Long-run:

The long run – the period of time when all factor inputs, including capital, can be changed.

5. Revenues (TR, AR, MR)

Total revenue – (TR) Total amount received from all units of output of a good, without regards to cost, profit, etc. units sold x price

Average revenue – (AR) The amount received in revenue from one unit of output without regards to cost, profit, etc. total revenue / units sold

Marginal revenue – (MR) The amount received in revenue from one additional unit of output without regards to cost, profit, etc.

6. Profit, sales & revenue maximization

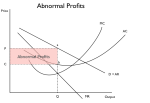

Profit maximization – the point where total revenue most exceeds total cost and marginal revenue is the same as marginal cost (MR=MC).

Sales revenue maximization – the point where the maximum possible revenue from the quantity sold is earned, where the marginal cost is zero (MC=0).

Sales volume maximization – the point where the maximum possible number of units is sold without incurring a loss. This occurs when average revenue is equal to average cost (AR=AC).

7. Perfect Competition

Definition:

Perfect competition – a situation in which no one firm has the ability to influence the market price of a given homogeneous product, with no abnormal profits sustainable.

Assumptions:

1) Many buyers and sellers. Nobody has power over the market.

2) Perfect knowledge by all parties. Customers are aware of all the products on offer and their prices.

3) Firms can sell as much as they want, but only at the ruling price. Thus sellers have no control over market price. They are price takers, not price makers.

4) All firms produce the same product, and all products are perfect substitutes for each other, i.e. goods produced are homogeneous.

5) There is no advertising.

6) There is freedom of entry and exit from the market. Sunk costs are few, if any. Firms can, and will come and go as they wish. There are no barriers to entry such as licenses.

7) Companies in perfect competition in the long-run are both productively and allocatively efficient.

Theory:

Abnormal profits are not sustainable. When a firm enters the market, it may be able to set its own price for the good or service, but sooner or later, recognizing the opportunity for some profits, a competitor would enter the market a lower the market price. This would repeat, with more competitors entering the market, until no abnormal profits are made by any participating firm, with only normal profits made.

8. Shut down and break-even price

The definitions:

Shut down price – the price where the firm can no longer sustain itself and, as a result, must immediately shut down.

Break-even price – the price where normal profits are made and, as a result, no more profits can be made.

The points on the graph / the equations:

Shut down price – point at which TR (Total Revenue) equals TVC (Total variable cost) and the product price equals its AVC (Average variable cost)

Break-even price – the point at which MC equals ATC (Average Total Cost). The break even price is the ATC.

9. Monopoly (elements of, model, theory)

The definition:

Monopoly – a situation in which one firm dominates the market. Other firms in the market must accept the market as established by those with monopolistic power, and therefore, these firms with monopolistic power are price setters. As a result, abnormal profit can be made in both the short and the long run. In the UK, a firm is considered a monopoly when it market shard is over 25%. Some industries can be considered natural monopolies, such as the water industry. A perfect monopoly occurs when there is only one supplier.

Assumptions:

1) Legal restrictions – a monopoly may be granted in the form of a patent, a copyright, or a license to do certain activities that are normally prohibited.

2) High capital costs – high barriers of entry due to large fixed costs in order to enter an industry may also result in a monopoly.

3) Limited sources of supply – certain products are only found in certain parts of the world and at certain times. If a certain country or firm controls these sources of supply, a monopoly can form.

4) Agreements between producers to limit competition – a number of firms may act as one entity and control the market for a product.

5) Non-price competition as a barrier to entry – the use of advertisements and branding may make it difficult for new firms to enter the market and as a result, a monopoly may form.

6) Tariffs and Quotas – to combat international competition, tariffs and quotas may be put in place so that domestic producers may dominate the market and a monopoly may form.

Model:

-A pure monopoly is when one firm controls the market for a product that has no close substitutes. However, they are very hard to identify in reality and therefore, we discuss the degrees of monopoly instead.

-Furthermore, the degree of monopoly may change depending on how narrowly an industry is looked at. For example, a city’s subway system may be a monopoly for underground transportation, but it is not a monopoly for public transportation in general.

-A five firm concentration ratio shows the proportion of an industry’s output produced by the five largest firms, and is usually used to determine degrees of monopoly.

Theory:

-The demand curve for the market in a monopoly will not differ from the demand curve of the firm identified as the monopoly. Therefore, the demand curve will slope downward, and will most likely be fairly inelastic as the presence of a monopoly implies that few substitutes are available.

10. Oligopoly (elements of, model, theory)

The definition:

Oligopoly – A market where there are only a few large firms. The firms have much dominance over any smaller starting firms, and therefore have a large amount of resources at their disposal, making the barriers to entry very high. Oligopolies can either be perfect or imperfect: in perfect oligopolies, firms make identical products while in imperfect oligopolies, firms make differentiated products.

Assumptions:

1) Limited number of firms – a few firms control the market for a given product

2) Dependence – the measures taken and the actions made by a firm have consequences for the firm itself as well as the market, oligopolies are commonly characterized by interdependence

3) High barriers of entry – entry into the market is generally difficult and costly

4) Product differentiation – usually the products are heterogeneous, or differentiated, and therefore have demand curves that slope down

Theory:

-Being large firms, although they benefit since the economies of scale become much lower, the diseconomies of scale are a major burden

-The oligopoly is a perfect oligopoly if few firms are producing an identical product while the oligopoly would be an imperfect oligopoly if the few firms are producing a differentiated product

-A duopoly is a type of oligopoly in which only two firms compete and control the market

-Oligopolies can be non-collusive or competitive if no collusion (definition in section “13. Forms of Collusion”) occurs, where the competition usually comes down to cut-price competition. However, if collusion does occur, the oligopolies are collusive oligopolies, where the competition usually goes down to non-price factors, trying to make the product itself better. Product differentiation occurs in hopes of attaining committed and loyal consumers, making a chief goal consumer loyalty.

11. Monopolistic competition (elements of, model, theory)

The definition:

Monopolistic competition – is when there are a large number of small firms who produce goods only slightly different from that of other sellers. There are low barriers of entry and abnormal profits can only be made in the short run as in the long run, profits will be competed away.

Assumptions:

1) Large number of firms – each firm has only a small portion of the market.

2) Independence – because of the large number of firms, the decisions made by each individual firm has little effect on all of the other firms.

3) Freedom of entry – anybody can enter the market.

4) Product differentiation – each firm produces a different good or service. Therefore, they have downward sloping demand curves.

Limitations of Model:

-Imperfect information

-Difficult to draw a demand curve for the entire industry

-Size and cost structure means abnormal profit can be made by firms in the same industry.

-Only focuses on price and output, but in reality factors such as variety of product and advertisement must be considered.

Theory (Efficiencies of Monopolistic Competition):

-Higher costs for firms but greater diversity for consumers.

-Less research and development and fewer economies of scale, but competition keeps prices low.

-Neither productive or allocative efficiency is achieved, but in the long run firms are closer to allocative efficiency and are productively inefficient.

12. Advertising and Branding

Advertising and branding – forms of methods that governments utilize to help influence an increase in the consumption of a good which brings positive externalities. These goods are often under-consumed, which prompts governments to intervene. Advertising can also be used to help influence a decrease in the consumption of a good. Such a good could be bringing in negative externalities. An example would be the consumption of tobacco. Governments can advertise the harmful effects to influence a decease in the over-consumption of this good.

13. Forms of collusion

The forms of collusion and their corresponding definitions:

Collusion – when two or more firms adopt policies to reduce or even eliminate the uncertainties associated with competition and begin cooperating with one another. Collusion may occur when firms wish to maximize their joint profits or to prevent new firms from entering the industry to maintain their current profits.

Cartel – where a small number of rival firms that sell a similar product come together to set an industry price and output in order to maximize profits for its individual members. Essentially, the firms in a cartel act as a single monopolist in order to achieve this goal.

Price leadership – when one firm sets a price that is subsequently accepted as the market price by the other producers.

14. Price discrimination

The definition:

Price discrimination – situation in which firms actively adjust prices according to the willingness or ability of different consumers to pay. This may depend on geographical, cultural, or other factors.

Necessary conditions:

1) The market must have some sort of imperfection since in a market characterized by perfect competition, no firm would be able to set their own prices.

2) The producer must be able to split the market into sections, and these sections must have no “seepage” – that is, one should not be able to sell the same product in one section to the other section

3) In each market, the price elasticity of demand must be different. This way, prices can be raised in the market with inelastic demand and prices can be lowered in the market with elastic demand.

Explanation / elaboration:

1st degree – charge whatever the market will bear e.g. auction

2nd degree – discount for quantity purchases

3rd degree – market separated into distinct groups:

-location

-time

-income

-age

-type

15. The kinked demand curve theory

Kinked demand curve: a theory created in order to explain the phenomenon in oligopolies where prices are relatively rigid even when costs increase. The model makes the assumption of asymmetrical reaction to a change in price by one firm; when one firm decreases prices, other firms will follow, but when one firm increases prices, other firms will not follow. This occurs because firms want to protect their market share as much as possible.

Written by: Thomas, Aron, Kestrel, Nick Lee, Eduardo, Shuichi, Jung-Hwan, Yuki, Keanu, Christopher, Rei, Michael